![[99%tech]](https://substackcdn.com/image/fetch/$s_!vl72!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fcae24093-688e-4321-a6fa-ee9385f8979c_1024x1024.png)

![[99%tech]](https://substackcdn.com/image/fetch/$s_!Sljl!,e_trim:10:white/e_trim:10:transparent/h_72,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F02f85460-45dd-47b2-a64c-f9e2bf0372af_1500x1000.png)

Two MBA students asked me separately for career advice. I was on a plane, so wrote them a long answer. I figured I’d share my thoughts here.

Venture capital is one of the best jobs in the world. It offers a rare combination: a high-level view into where technology and society are heading, paired with very practical exposure to how companies are built. You get to work with founders who are unusually ambitious, opinionated, and thoughtful about the future. For many people, including me, it is a dream job.

But it is not a career in the traditional sense.

Unlike consulting, banking, or operating roles, venture has no standardized progression. Getting an associate role does not imply a path to partner. Most venture firms are small and bespoke. They are optimized for investing, not for training or long-term career development. In fact, venture is often a poor place to learn the fundamentals of working. Judgment compounds slowly, feedback arrives years later, and it is hard to disentangle luck from skill. I’m almost 15 years into this and still trying to figure out if I’m good, hopefully great, or perhaps neither.

At the same time, venture can be an excellent launching point even if it does not work out long term. Many investors eventually become founders or operators, and the reverse is also common. But because there are so few seats, and because most firms are not designed to develop talent systematically, the opportunity cost of entering too early can be high.

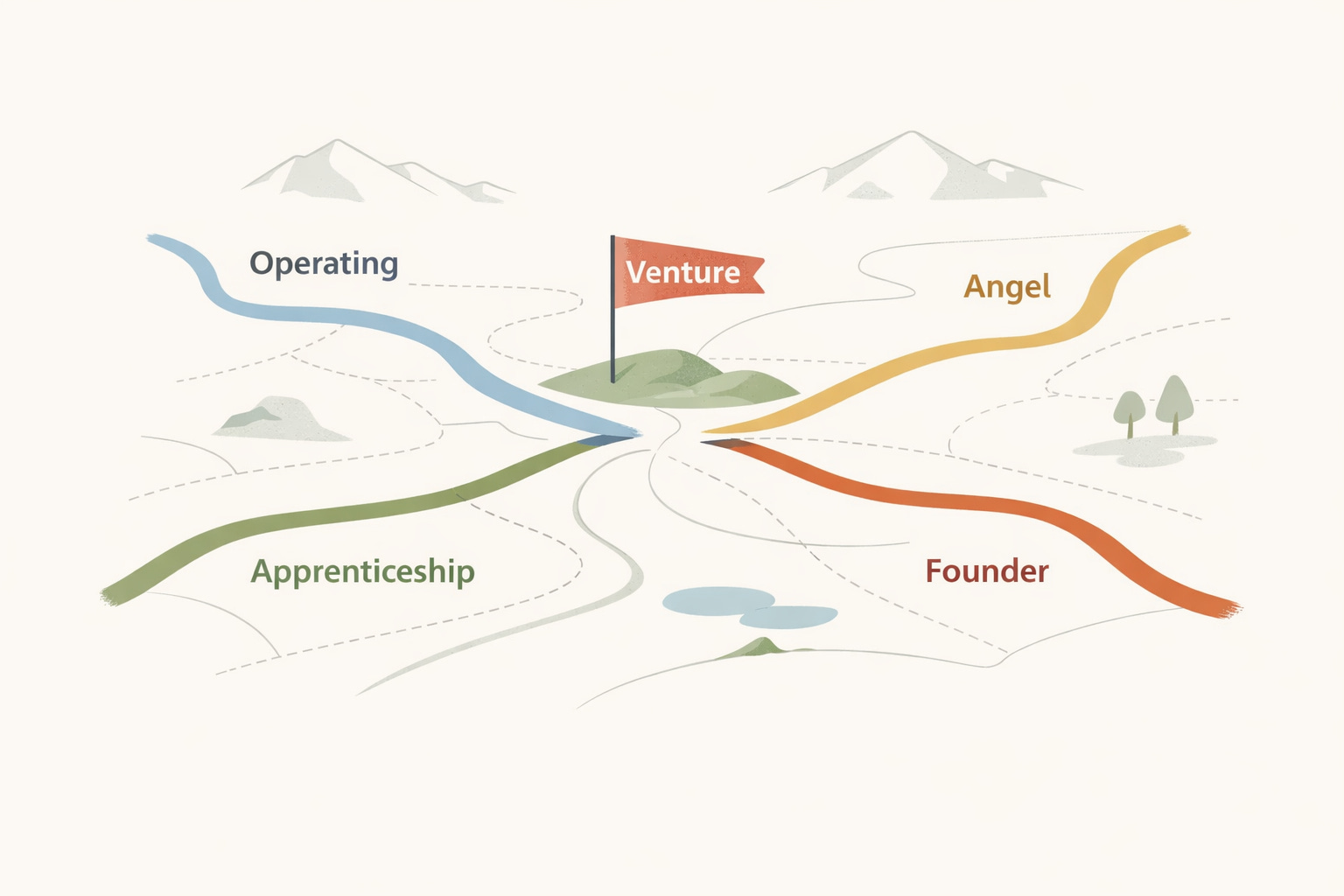

This is why I tend to frame the question less as “Should I do venture or operating?” and more as “How do I transform myself into a node for talent, with durable judgment and credibility?”

There are several proven paths into venture. Some come through a professional apprenticeship: investment banking, private equity, hedge funds, or consulting, followed by an associate role. This path works best early, when firms are hiring junior talent. Others arrive through operating experience, by founding a company or holding a senior role at a fast-growing startup where they develop real responsibility and credibility with founders. This is harder to pull off but often comes in at higher levels. A third path, increasingly common, is to start investing independently as an angel or through small syndicates, and to build a track record over time. None of these paths is inherently superior.

For someone in an MBA program, especially one with unusually high founder density, the more important question is how to test the work now rather than optimizing abstractly for a future role.

I usually suggest a simple set of experiments.

Develop a point of view. Effective investors are not generalists in the vague sense. They have a perspective on what is investable and why. When you meet investors, try to teach them something they do not already know, whether about a market, a geography, or a pattern they have not yet seen.

Start building relationships with funds you admire early. Funds are not hiring all the time. They hire when they have a need – either someone leaves or they raise a new fund and need to grow the team. Research which firms are in fundraising mode and focus your immediate application energy there. But don’t let this stop you from acting now on relationships. When it is time, you want them to call you first. Stay on it.

Build deal flow anchored in real relationships with founders. Many of the strongest companies of the last decade emerged from MBA cohorts, not because of the credential, but because of proximity, trust, and shared context.

Finally, try the work directly. Start investing, even in small amounts. Writing a first check is less about capital and more about learning, signaling intent, and building reference points. Platforms like AngelList let you build portfolios for fractions than it once cost. The goal is to build a track record and a unique perspective into the technology markets. Fellowships, part-time roles, or summer stints at venture firms are often the fastest way to understand whether the day-to-day reality matches the idea of the job.

Seek skills and experiences that compound regardless of whether you enter venture now or in the future. For most people, the best strategy is optionality: building skills and credibility that matter whether or not venture works out. The things that will make you a great young investor are the same as what might make you excellent in other professions – domain expertise, a unique network, strong work ethic, self-starting hustle, etc. Ironically, that approach is also what tends to make someone more attractive to venture firms in the first place.

Hi Alex! I think there's no standard path into venture. There's also the content creator path, where you develop deep domain expertise in 1 or 2 spaces to help a VC better understand them. I believe that those who thrive in venture usually have more than founder empathy and one superpower, such as sales, content creation, GTM, or anything of the sort, which can help them add value to the founder. For example, VCs from an investment banking background are financially savvy and thus could help the finance department of a startup, etc. I strongly believe you need operating experience because it makes you very distinct from others coming from different paths, as you're able to help the founder with day-to-day business operations.

I write a blog titled "The LegalTech Thesis", wherein I analyze startups, trends, and opportunities in the space. Would love to know your thoughts!

https://harshithviswanath.substack.com/