![[99%Tech]](https://substackcdn.com/image/fetch/$s_!Vpj7!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F288cd65c-980f-4acb-8182-1853ec1e444d_1280x1280.png)

The Future Of Venture Capital: Strategies That Win

Why Solo GP or Traditional Firm is the wrong question

This piece was first published on my Forbes column here.

Venture capitalists seem to always relish a debate. What’s better: Solo GPs versus partnerships? Small funds versus platforms? Large portfolios versus concentrated bets? Specialists versus generalists?

These questions resurface regularly on X — particularly when capital tightens and outcomes diverge.

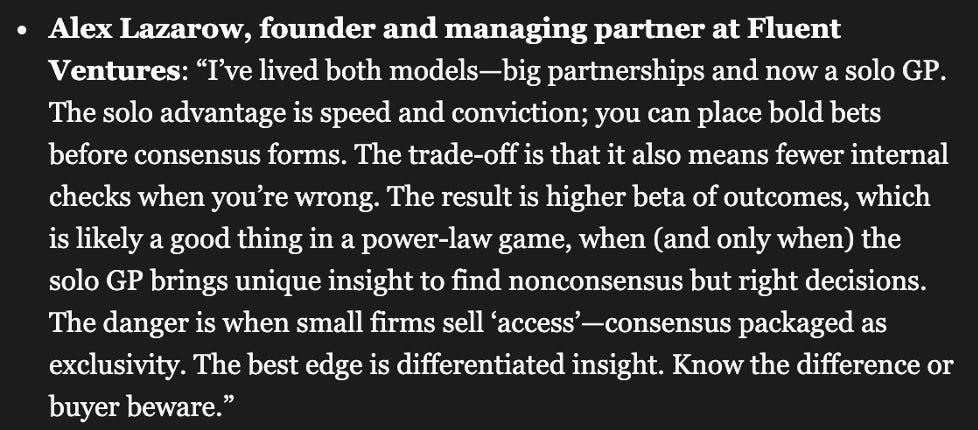

A few weeks ago, the Wall Street Journal posed a familiar version of this question: are solo general partners uniquely positioned to land explosive investments because they can move without the friction of consensus-driven partnerships?

My take, which I shared in the piece, is that it conflates a few dimensions. Partner count by itself is not the sole driver. What matters more is where an investor’s edge comes from, and whether that edge compounds over time.

The venture industry is evolving. I believe the next generation of outperformers - solo or otherwise - will not be defined by partner count, but how they deliberately play the game. Solo GPs have a few structural advantages for the new rules of the game.

Therefore, the question for today’s post: if there is a new game, then how does a VC win, and what strategies are most likely to be successful?

What Does It Mean to “Win” in Venture?

At its core, venture capital has a single scoreboard: distributed returns back to LPs (DPI). Everything else is a proxy, a leading indicator, or just noise.

The problem is that in venture capital, timelines are long, and getting to DPI can take a decade or more. Therefore, figuring out who is truly outperforming – over multiple vintages – is a challenging task in the short or medium term.

That’s why many performance metrics are leading indicators. They don’t correlate to DPI perfectly, and sometimes conflate success with noise. For example:

Fast mark-ups, which show genuine fundraising momentum, which is often associated with underlying revenue traction. But more rounds also means more dilution, and thus return compression.

Winning access or allocation into rounds is a proxy for competitive position in the moment. But if funds are winning access to hot rounds, the upside is often at least partially baked in with higher prices, which lowers the potential for multiples (just look at your favorite 100x revenue AI deal!)

Reputation and brand, which shape future access and founder perception. But if the reputation is relevant to the wrong audience, then it won’t drive returns, and worse divert fund resources and attention.

Return proxies matter, but they are not the same thing as performance. Many venture debates are really arguments about such proxies, not outcomes.

Four Strategies That Drive Venture Outperformance

Across market cycles, geographies, and fund sizes, my and Fluent Ventures’ (the firm I founded) view is that only four strategies consistently explain venture outcomes. They are slightly orthogonal. Though in some cases they can be combined.

1. Unique Insight: The Foundational Edge

A durable source of venture alpha is insight—the ability to see something before others do, or to understand it more deeply.

This can come from industry or thematic focus, sector specialization, geographic immersion, or lived operating experience. It shows up as pattern recognition, speed of conviction, and comfort acting before consensus forms. “Non-consensus but right” is not a slogan; it is the economic engine of power-law returns. These VCs offer their LPs differentiated and often uncorrelated returns to the market.

2. Unique Access: A Supporting, Not Primary, Advantage

Access plays an important role in venture and can come from founder networks, LP ecosystems, proprietary data, corporate partnerships, or embedded positions in specific markets.

Only 1% of companies ultimately become unicorns, and the best investors bat better on average.

Being in the room for as many of the 1% of companies as possible is critical.

Of course, and critically, access alone doesn’t drive returns. Selection and winning matter almost as much and in some cases even more.

A useful question for LPs and founders alike is not “who has access?” but “access to what?” Access to a narrow set of hot rounds is very different from access to broad, underexplored opportunity sets—particularly outside traditional innovation hubs.

3. Value-Add and Platform Capability

Over the past decade, value-add has evolved from a marketing claim into a genuine competitive dimension.

Talent networks, go-to-market support, executive recruiting, corporate development, and commercialization partnerships now shape how founders choose investors. Large platforms and some specialized firms have built impressive operating capabilities that can bend a portfolio’s company into a powerlaw.

Corporates and non traditional investors have an edge here too, by driving commercial success, increasing the company’s value (and presumably earning access).

4. Reputation (often tied to larger, storied, multi-stage firms)

Venture capital is one of the few financial products with returns persistence. One reason is that brand and reputation remain powerful forces in venture capital, begetting future access (and thus insights) into the changing technology landscape.

Yet reputation has a hidden cost. As firms scale and defend franchise value, strategies often migrate toward lower volatility and higher predictability. Or for sector specialists, get stuck into a strategy that used to work, but where the alpha has disappeared.

Where Solo GPs Fit, and Where They Don’t

Viewed through this lens, solo GPs are neither a panacea nor a liability.

The best solo GPs tend to excel at #1 and #2. Some bring deep, market-specific understanding. Others emerge from highly networked ecosystems and can tap into them quickly. Their defining advantage is decisiveness: the ability to act with conviction before a consensus forms.

And in a power-law game, this gives them the chance to find power-law returns.

From an LP perspective, solo GPs offer a different proposition: clarity. When an LP invests in a standard VC fund, they are picking the team. But, solo GPs allow LPs to create their own fantasy football team – choosing a few stars and building their own “dream” portfolio construction.

Imagine every VC portfolio didn’t have to be the Bulls vs. the Raptors. You could just build your own Team USA of superstars.

There’s always a but

Having worked within larger franchises for a decade before launching a solo-GP firm, there are structural advantages to larger firms, particularly around #3 & #4. Solo-GPs are just not set-up to offer the same level of platform benefits, and like any new firm, require a long time to build reputation. And of course, larger franchises can excel at #1 & #2 as well.

Another key nuance in my view, is that access alone is not enough. This is only proxy VC performance. The best solo GPs must have unique insights, to ultimately drive DPI performance that exceeds investing in a more generalist standard firm.

Strategy Over Structure

There clearly is not a single winning model. The venture firms that succeed over the next decade will not all look alike. But they will share one trait: a clear understanding of why they exist, where their edge comes from, and how that edge compounds.