![[99%tech]](https://substackcdn.com/image/fetch/$s_!vl72!,w_120,h_120,c_fill,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fcae24093-688e-4321-a6fa-ee9385f8979c_1024x1024.png)

![[99%tech]](https://substackcdn.com/image/fetch/$s_!Sljl!,e_trim:10:white/e_trim:10:transparent/h_72,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F02f85460-45dd-47b2-a64c-f9e2bf0372af_1500x1000.png)

The promise and challenges of embedded insurance

Reflections on my first in-person conference since the pandemic

This piece originally appeared in my Forbes column here.

Embedding financial products has been a buzzing topic in fintech and insuretech.

On the heels of Insuretech Connect (and a panel I moderated sharing the name of this piece), I wanted to share a few reflections on embedded insurance, where we are today and where the sector is going.

First, what is embedding financial products, and particularly insurance? It can range on the one end from using novel distribution channels to sell existing products in new ways (e.g. getting your title insurance for your home as part of your online mortgage refinancing with companies like Spruce), to much deeper embedding (and where I think the most exciting innovations will come from in next few years) where the product is a feature of your purchase (e.g. a Tesla includes the car insurance when you purchase it).

In this piece, we explore a few drivers for the movement, where we’ll see adaptation and what dislocations are coming.

Drivers for embedded insurance

The rise of embedded financial products has been well documented. One of the key reasons is that embedded products can strongly leverage the “3Ds” of fintech. They enjoy a distribution advantage because they can be purchased where customers are, and with brands they trust. They can become features of a product rather than something that is separately bought. They can leverage different types of data for underwriting and claims. And because they are part of a broader offering, can delight the customer in the delivery.

My favorite example is ZhongAn phone insurance, embedded in phones – before you pick up your dropped phone with a cracked screen, the embedded policy will have been triggered by internal sensors and a new phone will be on its way. No messy claims or repair estimates needed.

This is a powerful shift but not the only driver for the movement.

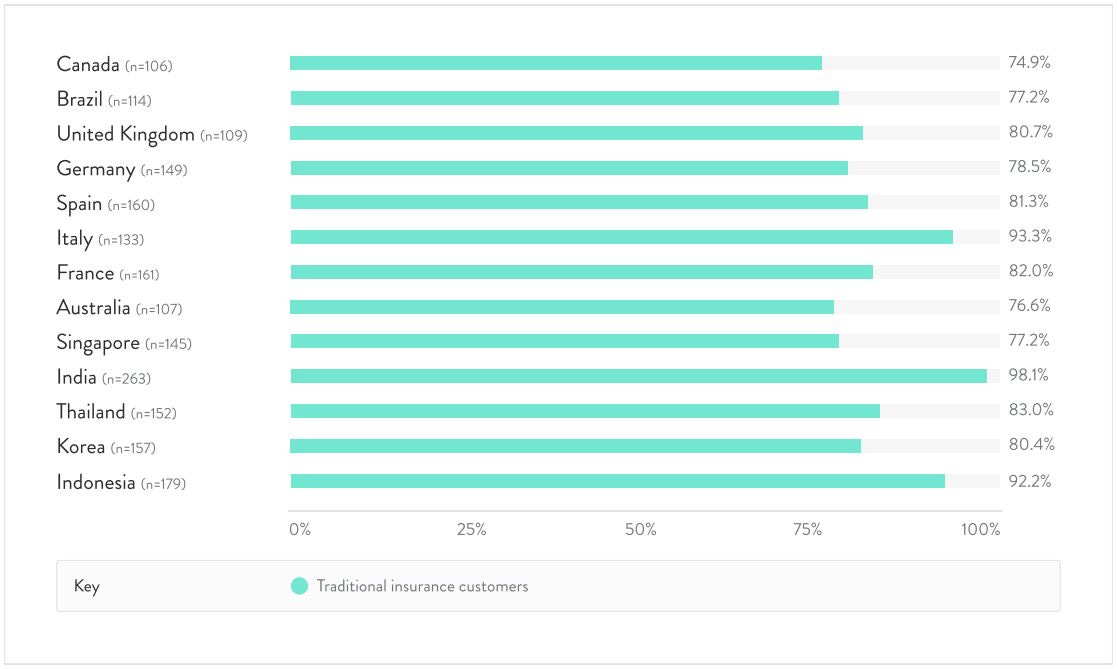

Embedding products is increasingly popular with consumers. Research by Cover Genius, an embedded insurance provider, unveiled during our panel demonstrates this dynamic at work. Findings showed that 45% of US customers are interested in bank-embedded insurance offers. Strikingly, globally the average is even higher, reaching 70%.

Perhaps most striking, compare this with global research that suggests that 64% of consumers have tried a fintech product. This suggests that there is a huge potential to drive adoption and adaptation via embedded channel, not necessarily from dedicated fintech brands.

Lastly, embedding financial products offers an opportunity to increase the total addressable market. The old adage goes: “insurance is not bought, it is sold”. The rub is that it is hard to sell insurance. But if purchased at the right moment, it becomes easier. Executed well, new categories of insurance can be created.

This is good news to the over 1.5 billion people who have no bank account (nearly the same amount that are underbanked). This may explain the much higher willingness to try new embedded insurance products in underserved markets – India was 95% and Indonesia was 76% - because existing options simply do not serve the customer base. Embedding financial products is one way to lower the cost of serving customers – in this case by making onboarding and reaching customers much cheaper, and shared with a partner or another business line. These may prove one tool in driving financial inclusion.

Reinvention is required

The shift toward embedded insurance is not as simple as shifting the distribution channel.

Quite a lot needs to change. As Chris Pedak from LAMIE a European embedded insurtech focusing on telcosurance explained during our panel, his objective is to get to 100% claims paid out (they are presently at 98.7%, with an NPS of 80+, and 70+ with those they declined). This does not happen on its own. For this to work, the entire product – from the coverage, to the claims process needs to be rethought.

Embedding financial products requires simple clear product, with simple clear explanations. Descriptions need to be in plain English, rather than complicated legalese. And products will need to shift away from exclusions to be more understandable and viewed with greater trust.

Embedded insurance forces us to rethink claims as well. Here, we’ll see greater use of parametric triggers – where a certain event, which is easily measurable – triggers the claim. It becomes indisputable, and as a result can lead to 100% payouts. For instance, parametric weather insurance that pays out based on events, or screen insurance that triggers based on internal phone sensors.

This also means that some products are easier to embed than others. Products that require complicated underwriting (think life insurance where health and behavior factors are big underwriting drivers), that require an understanding of customer behavior and moral hazard (e.g. Cyber where customers have an important role in prevention) or where many exclusions are present, may be more challenging to embed.

Dislocations are coming

Embedding financial products has the potential to rearrange the chairs in insurance.

For one, what is the role of traditional carriers or agent distribution networks? In this new model, insurance can be distributed through new channels or bundled into a product experience. The insurance balance sheet does not need to come from a traditional insurance provider – instead it can be purchased from reinsurance providers or the market (insurance linked securities).

If certain categories are dominated by embedded insurance, say warranties, other areas will be left out. New types of policies will be required – like expanded umbrella coverages.

Lastly, embedded insurance is an area that shows the growing trend of globalization of fintech. Many platforms in the space are multi-country from the get go. Cover Genius is present in over 60 countries, LAMIE is active in eight countries. Because they often partner with platforms they get pulled into multiple markets rapidly. Embedded insurance players thus need to manage the complex and often thorny regulatory landscapes across markets. But once they do, it is possible to move quickly to scale.

So, where are we now?

I believe we are still in the second inning of embedded insurance adoption. The first wave saw a shift in distribution players. Today we’re seeing the beginnings of embedding it in platforms and others, and making insurance a feature of a product.

I expect that next year’s ITC will have many more examples of products in embedded space. But five years from now, it will be a powerful (though not universal) approach to insurance.